Here’s my annual review of what’s trending for the in-destination experiences industry. I especially like to take a look back to see how I thought things were trending at the end of prior years compared to how I see things going into the next year.

Why “Back to the Future”? Because travel is back, all the way back to 2019 levels and in many ways already ahead. And with Asia and China now poised to come back, travel in 2024 and beyond will continue to grow to levels originally forecasted in 2019. Buckle in, the best is yet to come for in-destination experiences, 2024 is going to be a great ride.

I think my 2021 and 2022 lists were pretty spot on. Here’s my current thinking as we head to 2024: let me know what you think!

Eight of my Top Ten from December 2021 were on the list in 2022, but that’s now down to only four. What’s gone? Timed ticketing (it’s no longer a trend, but a good outcome from Covid), Hiring and Training (we can argue this should definitely still be on the list, but again, I don’t think this is a trend but an ongoing result from Covid), Follow the Money is off the list (but over $400M did go to two OTAs referred to in #5) and Local and Covid are also no longer on the list. (Local is another one of those things that remains critical, including local groups, but no longer a Top Ten Trend.) Self Guided Tours and Tech is back after being off the ‘22 list, as part of #1.

And now for the end of year 2023 Top Ten Trends and comparisons to 2021 and 2022:

| Dec 2021 | Dec 2022 | Dec 2023 | |

|---|---|---|---|

| 10 | Timed Ticketing and Attractions Tech | Attractions Tech | Outdoors Rules |

| 9 | Hiring and Training | DEI and Sustainability | Immersive Experiences |

| 8 | Immersive Experiences | Local | DEI and Sustainability |

| 7 | Adventure and Outdoor Rules | Outdoors Rules | Less Trips, More Experiences |

| 6 | Follow the Money | Follow the Money | Dynamic Pricing |

| 5 | DEI and Sustainability | Generative AI / ChatGPT | OTAs Continue to Dominate Growth |

| 4 | Self Guided Tours and Tech | Immersive Experiences | Experiences Driving Destination Choice |

| 3 | Google Things to do | Hiring, Training, Retaining | Short Form Video |

| 2 | Local | Short Form Video | Google Things to do |

| 1 | Covid-19 | Google Things to do | Generative AI: A. Content Generation B. Customer Experience C. Multimodal Immersive Tours |

30 September – 3 October 2025

Insider Pro Access Members Save 20%

THE event of the year for solutions-focused In-Destination Experience creators and sellers

Get Your Spring Savings Ticket Today!

10. Outdoors Rules

From #7 to #8 to #10 this year. Interest in the great outdoors continues to grow. The pandemic effect that pushed more people to participate in outdoor activities will be an ongoing trend.

9. Immersive Experiences

Immersive Experiences, what does that even mean these days? Everyone says their experiences are immersive. Like last year when I had Immersive Experiences at #4, I’m still not talking about AR or VR or the Metaverse. I mean attractions as well as tours that create immersive experiences.

Still one of the best examples, and now growing with two new locations in Texas, is Meow Wolf, whose mission is to “Inspire creativity through art, exploration and play so that imagination will transform the world”. The opening of The Sphere in Vegas this year truly rocked the world of immersive experiences featuring U2 concerts and a variety of amazing immersive experiences. Here’s a great list of The World’s Top Immersive Art Experiences from Blooloop.

Immersive Experiences are also being created by companies like Imagine Experiences featuring their Bond for a Day experience and, of course, all of the operators who are working hard to create authentic experiences where travelers get immersed into the local community.

8. DEI and Sustainability

I have to keep Diversity, Equity and Inclusion (DEI) and Sustainability on my list. Although I wish there were really significant changes happening, there haven’t been anything that I can really point to here at the end of 2023. But these remain topics our industry must keep front and center, and the increase of climate- and weather-related emergencies impacting tourism this past year and forcing tour operators to adapt underlines the importance of prioritizing sustainability.

Our industry must support organizations like Tourism Diversity Matters, Sustainable Travel International, Leave No Trace, The Untours Foundation and companies led by entrepreneurs from marginalized communities and companies that support the economies of the local communities in their destinations (here’s one great example) who produce tours focused on cultural heritage.

7. Less Trips, More Experiences

US Travelers took less trips in 2023 than 2022, but, but they are making the most of those trips. Experience travelers reported doing an average of seven experiences on a trip in 2023. This includes an increase from 2.7 tours per trip in 2019 to 4.7 tours per trip in 2023 – wow, think about that. That is a huge difference. These travelers are taking fewer trips, but spending more per trip.

6. Dynamic Pricing

Last year, I had Attractions Tech as #10 on the list. This year, I’m focusing specifically on dynamic pricing for attractions. The tech is there (although still somewhat limited) and attractions are ready to get on the bandwagon of dynamic pricing that has already been standard operating procedure for airlines, hotels, and even music and sporting events for years.

The hardest question that remains is for dynamic pricing that operators are using for direct bookings to be ingested (accepted) by the OTAs and other distribution partners. This is primarily a factor for enterprise experience operators, but over the next few years will become more and more important for all experience operators and ensuring a sustainable bottom line. (Note: variable pricing is not dynamic pricing – learn more about both here.)

27-29 April 2026

Insider Pro Access Members Save 20%

THE event of the year for the European in-destination experiences industry

Get Your Super Early Bird Ticket Today!|

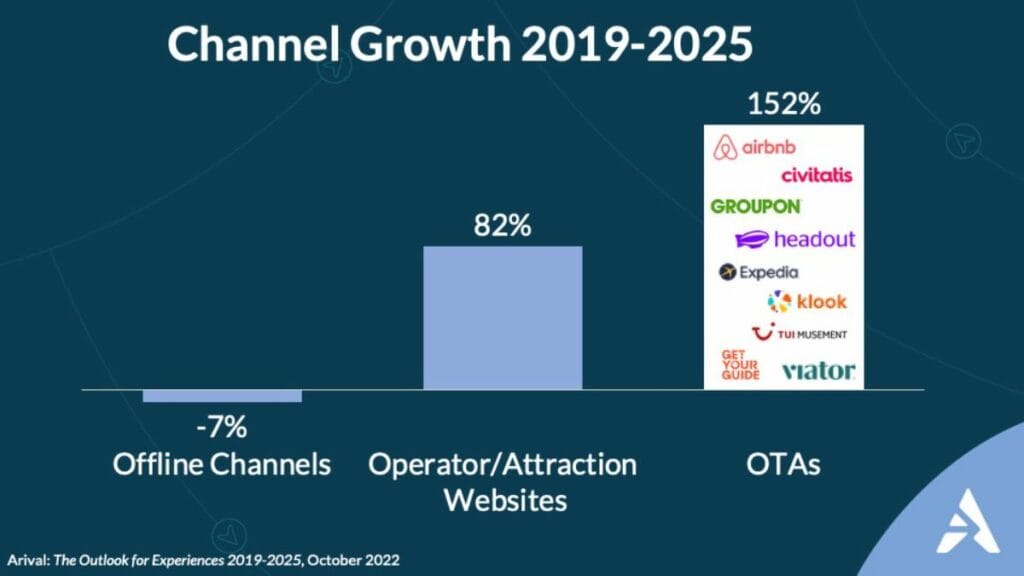

5. The big OTAs keep getting bigger

Online travel agencies (OTAs) continue to be the fastest-growing sales channel in tours, activities and attractions, dominating growth in the experiences sector, and the biggest OTAs keep getting bigger.

- In Asia, Klook reached profitability in 2023 and raised an additional $210M, bringing their total funding to $932M.

- In Europe, GetYourGuide announced in May that they raised an additional $194M at a $2B valuation (double their valuation in 2019!)

- Viator, meanwhile, continues to be the largest Global OTA by a long shot and remains the dominant player, reaching $1.1B of gross bookings in both the second and third quarters of 2023.

4. Experiences are Driving Destination Choice

Forty-nine percent of Gen-Z and Millennial travelers say experiences – tours, activities and attractions — have a significant role in their decision on where to go on their trips. Historically travelers have planned and booked their tours, activities and attractions close to trip departure or usually in-destination itself, and almost always after organizing the transportation (e.g. flights) and accommodations.

But this is changing (and fast). More and more, younger travelers are choosing destinations based on what they want to do, including events (sports, music, shows, festivals), attractions and other experiences, and booking these experiences in advance. (Look for our forthcoming report on The Power of Events for an exploration of the key trends and insights around events-based travel.) This is a huge opportunity for experience creators to take advantage of.

3. Short Form Video

Still in the top three, Short Form Video, led by YouTube, Facebook, Instagram and TikTok, continues to grow as the top of the funnel for travelers during the dream and inspiration phase as Arival’s 2024 U.S. Experiences Traveler study illustrates.

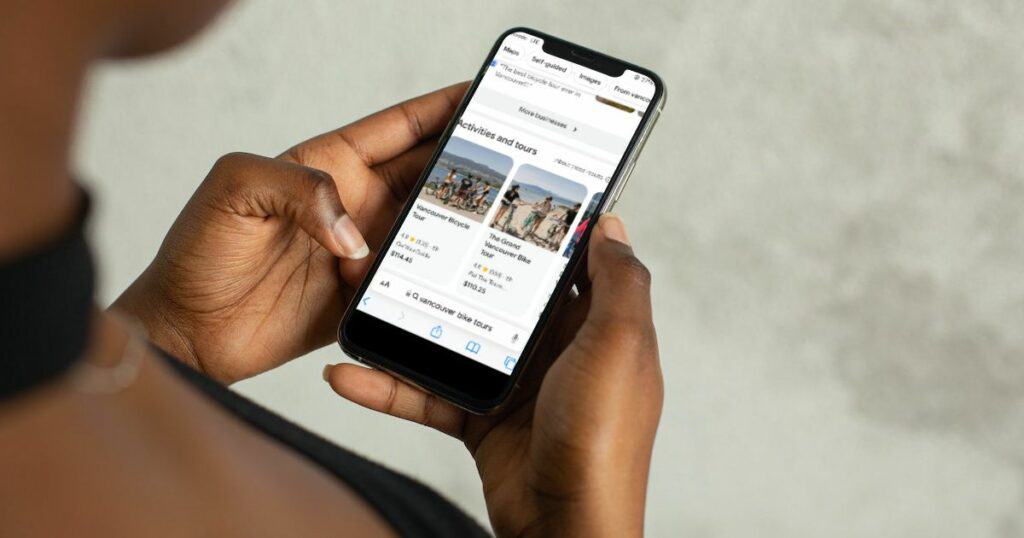

2. Google Things to do

Dropped from #1 in 2022, but still up from #3 in 2021, Things to do remains the operator’s best friend for direct bookings. But only if they understand how to take advantage of the product to drive direct bookings. OTAs are still dominating bookings through Things to do. Our number one piece of advice for 2024 is, if you’re not already leveraging Google Things to do for your experiences, make that your #1 priority for 2024. Let us know how we can help you!

- Marketing With Google: See the latest Google info on Arival, from on-demand sessions to articles and updates about Google Things to do, compiled in one place.

- Google Things to do Support Page: Google’s info page for Things to do.

- Here’s an excellent resource from our friends at Magpie Travel. Magpie is one of Google’s Connectivity Partners and is always on top of Google’s updates.

1. Generative AI

Number one of course is Generative AI. But not just number one, really, I’m putting GenAI as number 1, 2 and 3. But since I have other categories I have to include in the top 10, I’m listing GenAI as number 1A, 1B and 1C.

A. Content Generation

The most common use of AI for in-destination experience creators today, with Text-to-Image and multimodal capabilities, AI will continue to drive innovation and capabilities in content generation. For example: Enter a prompt to create images, such as photos, artwork, charts, logos, etc. These models – and various tools built on these models – have come a long way in 2023. Here is an example of an image created using Bing Image Creator, courtesy of my good friend Christian Watts.

Prompt: “Modern red hop on hop off open-top double decker sightseeing bus in Dublin. Bus is full of happy tourists sitting down. Blue sky with white fluffy clouds. Brand is Dublin Tours.”

B. Customer Experience Pre/During/Post Trip

AI applications are helping to enhance customer interaction through automated messaging, email, live chat, however a company chooses to communicate with their customers (and staff). AI can also help enable more reviews, cross sell and more. This is my prediction for the area where AI will have the most impact for experience creators in 2024. What sounds better than improving CX while reducing costs and creating efficiencies?

C. Multimodal to Create Immersive Self-Guided Tours

Multimodal is the GenAI for images, audio and video. Platforms for self guided tours are being developed, Autoura for example, where customer experiences are hosted and guided by AI tour guides. The experiences are multi-lingual and are walking or vehicle-based. The AI guides can deliver information, answer questions from the customers and personalize the content based on customer preferences. Use cases include self-guided audio tours, (city, museum, walking, driving tours, etc.) translation guides for tour guests who prefer a different language, or very niche tour experiences which may not be economical to run with a human guide, among other examples.

Look to 2024 and Beyond with Arival

Join us in March for the first Arival event of the year at Arival 360 | Berlin, where we’ll gather industry leaders, experience operators and other experts to discuss the top trends in in-destination experiences and practical strategies that position your business for success in a rapidly evolving landscape.

Become an Insider Pro Access member today and get access to the full library of Arival research, plus many other benefits such as free consulting sessions, special discounts and 20% off in-person events, starting from $179 per year.

Sign up to receive insights tailored for the in-destination industry as well as updates on Arival.

Header photo: Pexels / Carlos Lopez